Equity Methode Beispiel

Beispiel zur kapitalkonsolidierung nach der equity accounting methode.

Equity methode beispiel. In such a case investments are accounted for using the cost method. When a company owns more than 50 but less than 100 of a subsidiary they record all 100 of that company s revenue costs and other income statement items even. For businesses the amount of money capital invested by the owners of the business in order to buy various assets it is also referred to as owners equity. This method is used when the investor holds significant influence over the investee but does.

Anteiliges nicht neubewertetes bilanzielles eigenkapital des anteilsunternehmens. Schema equity methode nach buchwertmethode. Der einfachheit halber sei angenommen dass das vermögen der a gmbh zum 31 12 01 lediglich aus anlagevermögen mit einem buchwert von 500 t besteht. Die gewinne und verluste dieser betriebe wirken sich damit unmittelbar auf die konzernbilanz des investors aus was die equity methode vom rechnungslegungsverfahren nach dem anschaffungskostenprinzip unterscheidet.

Equity financing has various advantages both to the founders and to the investors. What does equity method mean. The company does not have enough cash collateral or resources to raised funds from debt financing hence equity financing is a good source of funds for the entrepreneur as the investors would take risk of the business along with the founders. Unterschiedsbetrag beteiligungsbuchwert abzgl.

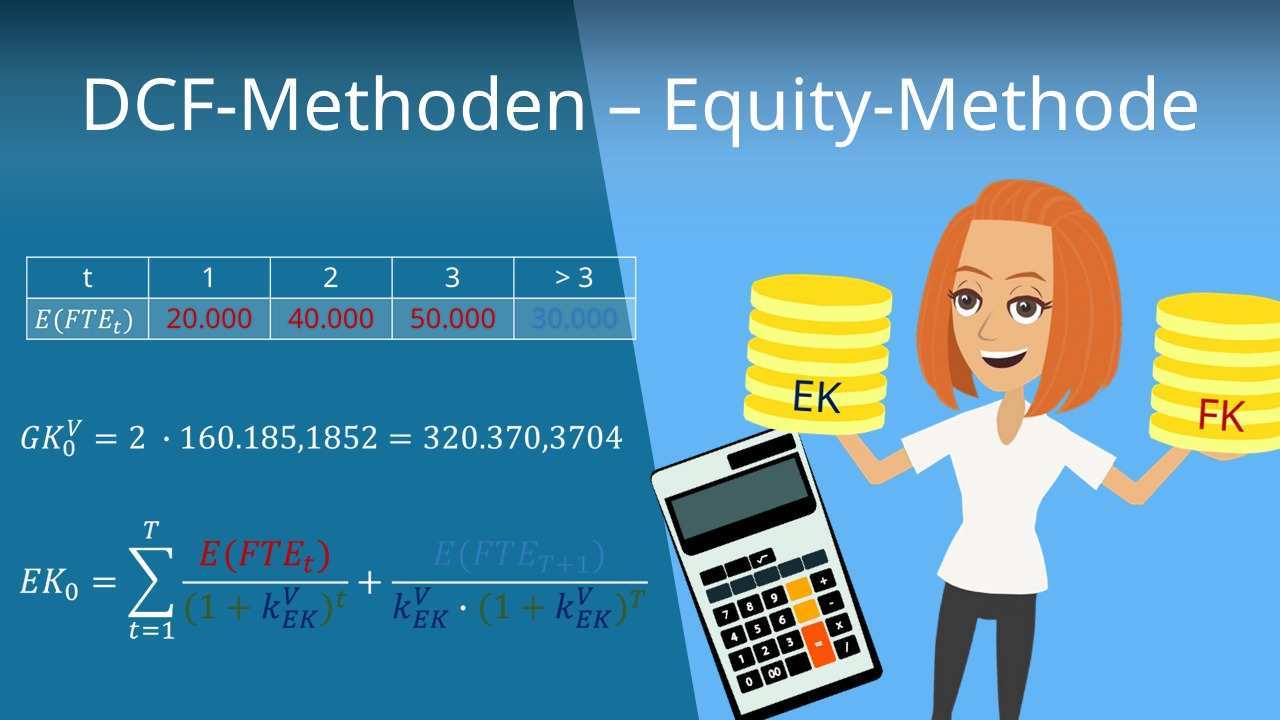

This makes sense because if the investor has significant influence over the investee they could be considered the same company. The investor becomes the parent company and the investee becomes the subsidiary company to the extent of the investment. Gegeben sind die erwarteten variablen flow to equity eines unternehmens für den zeitraum t 0 bis t 3 und die konstanten erwarteten flow to equity für alle perioden t größer 3. The equity method is a type of accounting used for investments.

Die equity methode ist eine spezielle form der rechnungslegung bei der konzerne bestimmte beteiligungen an unternehmen in ihrem konzernabschluss berücksichtigen. The term shareholder s equity is generally used for registered companies where shareholders basically are the owners of. Die m ag ein automobilbauer erwirbt zum 31. Schauen wir uns das mal an einem beispiel an.

Anteilige stille reserven anteilige stille lasten und. Berechne den unterschiedsbetrag durch. For individual equity is determined by ownership in house and car. Die muttergesellschaft hält 30 der stimmrechte und des eigenkapitals des assoziierten unternehmens.

Die erwarteten flow to equity sind 20 000 40 000 50 000 und ab t größer 3 gleich 30 000. Dieser unterschiedsbetrag lässt sich verteilen auf.